Nintendo has been facing an incredible amount of pressure from existing and new entrants to the gaming space that has led to a decline of its market share. With only so much time in one day to consume media, consumers have a choice between “core” gaming, by way of consoles and PCs, and a more casual experience via browser and on mobile devices; Nintendo has found itself at the service of neither audience.

With the impending launch of Wii U, the company has taken a public stance in support of the core gamer, but is faced with overcoming the challenge of offering a superior online experience to the established leader in the space, Microsoft and its Xbox 360. Its track record with Wii Shop leaves many of us doubtful that it can rebound in this sense. Meanwhile, the mainstream audience that helped propel Nintendo to success in the last decade with the Wii is being abandoned in favor of more costly hardware and complicated controls of the Wii U.

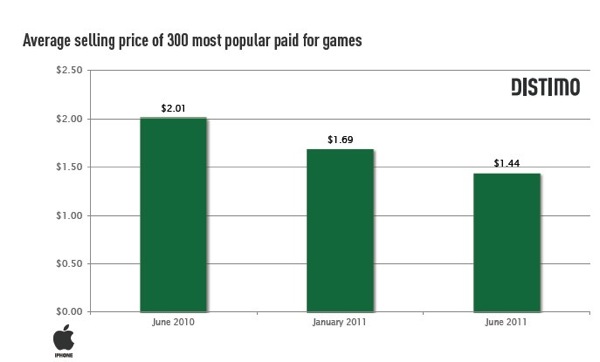

Clearly, Nintendo’s platform is at risk of failure, and investors and Mario fans alike are clamoring for a shift in strategy. Most notable among the call for action lies with the leader and renowned innovator in software and hardware – Apple. Prior to iOS, we had terrible interfaces that were counterintuitive to driving engagement of content and considered a 5% market penetration of games as a success. Since the debut of iOS and the App Store, we’ve seen the market expand to over 600,000 applications and indie developers rising to fame, claiming thousands in revenue, and in some cases millions. Google Play trails closely behind with over 500,000 applications available, although the platform faces piracy issues that leave it second to iOS in terms of developer support.

The new market opportunity is in mobile gaming, as Apple and Google continue to seed global audiences with smartphone devices that spur user engagement with various forms of content, most notably games. Should Nintendo bow to market pressures and take Mario, Zelda and Metroid to mobile devices? Certainly not now, without sacrificing its entire platform and affecting its remaining grip on the game enthusiast market. Let’s analyze the implications of what can be seen as a rash decision in several ways.

Shifts in Revenue

Nintendo’s revenues have taken a hard hit as a result of our shift to mobile platforms. Wii owners are largely content with Wii Sports, and those mainstream consumers have hardly converted into purchasers of additional software, resulting in decreased developer support. The 3DS launched to a cold welcome, but has since slashed prices and achieved moderate success among a stagnant core gaming audience.

The company recorded its first operating loss of $460 million for fiscal year ending March 31st, much of which can be attributed to the struggling Wii console, DS and 3DS, all falling short of sales expectations and incorporating price cuts in response to increased competitive pressures. We can also assume that much of the capital was allocated to continued support for game developers on each platform and R&D towards Wii U.

The company recorded its first operating loss of $460 million for fiscal year ending March 31st, much of which can be attributed to the struggling Wii console, DS and 3DS, all falling short of sales expectations and incorporating price cuts in response to increased competitive pressures. We can also assume that much of the capital was allocated to continued support for game developers on each platform and R&D towards Wii U.

Meanwhile, Rovio released its 2011 earnings statement, highlighting $67.6 million in profit on $106.3 million in revenues that can be largely attributed to its Angry Birds property, 30% of which came from merchandising and licensing. Based on these numbers, we can estimate that around $70 million was generated by downloads of Angry Birds. Impressive numbers indeed and deserving of praise for the company’s immense success across the various platforms on which Angry Birds can be found.

Yet, Angry Birds is at the top of the food chain, and few (if any) can come close to matching the success that Angry Birds has seen. And in comparison to Nintendo’s current business, it fails to match the numbers of its own game platform business.

For fiscal year beginning April 1, 2012, Nintendo is expected to achieve $500 million in operating profit according to a forecast estimate compiled through a survey of 20 analysts by Thomson Reuters I/B/E/S. The company controls its own fully integrated platform specifically tailored to gaming, similar to Apple’s hardware/software strategy that spans personal computers and mobile devices, not to mention the impending launch of the rumored iTV. Nintendo sells the hardware and controls the pipeline of software making its way to consumers, consisting of its own popular IP and an ecosystem of developers from which it generates additional revenues with every game purchase.

Let’s take a look at another example, one that would be on the lower end of Nintendo’s sales figures on a platform that is largely characterized as “struggling” – Mario Kart 7 on the 3DS. The title has so far achieved global sales of nearly 5.5 million units, running at $39.99 a pop. That’s nearly $220 million in revenues, over double Rovio’s business. Now, the margin on packaged goods isn’t really as significant, but even if we’re looking at a 20% profit margin, we’re talking about approximately $44 million in profit from a single title that has been on the market for only 6 months and on hardware that isn’t even considered a mainstream success. Looking forward, it’s not a stretch for Nintendo’s hardware to go strictly digital as industry trends indicate and eliminating the packaged goods channel, increasing margins and generating even greater profits (considering a premium price point maintained through “deeper” gaming experiences of Nintendo hardware). Also, this is just for one title – consider all the other games moving through the 3DS, controlled 100% by Nintendo and generating even greater revenues from both 1st and 3rd party games.

Let’s take a look at another example, one that would be on the lower end of Nintendo’s sales figures on a platform that is largely characterized as “struggling” – Mario Kart 7 on the 3DS. The title has so far achieved global sales of nearly 5.5 million units, running at $39.99 a pop. That’s nearly $220 million in revenues, over double Rovio’s business. Now, the margin on packaged goods isn’t really as significant, but even if we’re looking at a 20% profit margin, we’re talking about approximately $44 million in profit from a single title that has been on the market for only 6 months and on hardware that isn’t even considered a mainstream success. Looking forward, it’s not a stretch for Nintendo’s hardware to go strictly digital as industry trends indicate and eliminating the packaged goods channel, increasing margins and generating even greater profits (considering a premium price point maintained through “deeper” gaming experiences of Nintendo hardware). Also, this is just for one title – consider all the other games moving through the 3DS, controlled 100% by Nintendo and generating even greater revenues from both 1st and 3rd party games.

For Nintendo to trash its own closed gaming platform for Apple’s in pursuit of revenues that have not publicly achieved the scale that Nintendo currently maintains just doesn’t add up. It’s also understandable that Nintendo derides the thought of having to pay Apple the 30% cut, which would make it an even greater challenge to achieve success on the scale of its current games business. A counter argument to this is that Nintendo can offer games on each platform, which doesn’t come without merit, but let’s take a look at this audience.

Can Mario Wear Different Hats?

For Nintendo to reach the scale of success on Apple’s platform that it currently achieves within the confines of its own closed platform, let’s assume two scenarios: 1) that the game experience is rich enough to sell on the level of Angry Birds (that’s 1 billion downloads!), or 2) that Nintendo sells at a premium with less market penetration. Both situations would have to involve the creation of new games based on its popular IP, rather than a direct port of old games which would only have a minimal impact on Nintendo’s bottom line, not to mention potential disappointment in the controls for some of our most favorite classics that were built for console controls.

For Nintendo to reach the scale of success on Apple’s platform that it currently achieves within the confines of its own closed platform, let’s assume two scenarios: 1) that the game experience is rich enough to sell on the level of Angry Birds (that’s 1 billion downloads!), or 2) that Nintendo sells at a premium with less market penetration. Both situations would have to involve the creation of new games based on its popular IP, rather than a direct port of old games which would only have a minimal impact on Nintendo’s bottom line, not to mention potential disappointment in the controls for some of our most favorite classics that were built for console controls.

The first scenario would be largely targeted at the expanded mainstream audience, one that Nintendo did a great job of penetrating with the Wii and DS. Yet, we have to ask ourselves if the casual gamer of an older demographic and one that skews female would be willing to purchase a Nintendo device if Mario could be had on an iPhone, iPod touch or iPad. Facing limited time in one’s day, chances are that this gamer would skip the purchase of a game-dedicated device and invest $0.99 on a more casual Mario experience. Asking my wife and her 21 year old sister if they’d purchase a new Mario for Wii if they had Super Mario World on their mobile device, they both confidently answered “no way, the app would be good enough”. This would affect the purchasing decision of millions of consumers and cannibalize Nintendo’s gaming platform at a much more significant loss than what it can possibly recover in $0.99 downloads. This isn’t a risk that Nintendo can afford to make, at least not right now.

The second scenario involves a very challenging balancing act of pricing games at a premium, say $9.99, and selling through enough downloads to generate a return on development costs. This would carry an even greater risk of cannibalizing Nintendo’s own platform as these premium games would also come with a deeper and richer gaming experience that could potentially directly compete with Wii U, DS and 3DS game quality. If I have a great Mario title on my mobile devices at $9.99, chances are that I’ll skip the dedicated hardware and $50 price tag for the game.

Additionally, either decision would send a very negative signal to the remaining developers who still believe in Nintendo’s gaming platform, causing additional speculation about those consoles’ impending demise, an even further loss of support in game development, and all but hammering the final nail in the coffin of Nintendo’s platform.

Finally, do we really want an innovator in the gaming space to drop what it does to hop on the iOS bandwagon and solely rely on a touchscreen interface? Is the future of gaming really only about the touchscreen, perhaps with gesture and voice recognition integrated within? Imagine where gaming would be now if Nintendo bowed down to economic pressures back when the GameCube was being labeled as a failure and the Wii and DS never happened. All those Wine, Cheese and Wii parties would have never happened, and one could fairly assume that the Kinect and Move gaming experiences may not have been inspired into market release, perhaps confined to TV integration and never having impacted the games we play.

“Tiiiime Is On My Side, Yes It Is”

Mick Jagger’s voice resonates in my head as I read that Nintendo is sitting on a pile of cash amounting to $14 billion. Not only is Nintendo expected to turn a profit for fiscal year 2012/13, but it has a war chest to conceive and define the “next generation of gaming” through a fully integrated hardware and software platform, one that’s made exclusively for gamers and consumers seeking a good time. Even though the new Wii U doesn’t spur much hope with industry analysts and other market players, such efforts would be completely lost if confined solely to the hardware and interface design choices of Apple, a company whose business is far greater than the games sector to justify a focus on giving us new ways to experience video games.

Mick Jagger’s voice resonates in my head as I read that Nintendo is sitting on a pile of cash amounting to $14 billion. Not only is Nintendo expected to turn a profit for fiscal year 2012/13, but it has a war chest to conceive and define the “next generation of gaming” through a fully integrated hardware and software platform, one that’s made exclusively for gamers and consumers seeking a good time. Even though the new Wii U doesn’t spur much hope with industry analysts and other market players, such efforts would be completely lost if confined solely to the hardware and interface design choices of Apple, a company whose business is far greater than the games sector to justify a focus on giving us new ways to experience video games.

But how much time does Nintendo really have to make a decision? Even with $14 billion to cover years of operating costs, Nintendo can’t afford to sit around forever. A fair guess at the amount of time that Nintendo has to evaluate the marketplace and give a shot at maintaining a unique gaming experience lies perhaps in the 5-10 year range. Most everyone will understandably argue that this is too much time, but Mario, Zelda and Metroid aren’t going anywhere, and if Nintendo’s own platform faces a demise there will always be an audience ready to pounce on these titles when made available on iOS, Android or any other platform outside the company’s own walls.

Atari, who is celebrating its 40th anniversary this year, has hit a milestone of 10 million downloads just a year after releasing a number of classic and new games based on its renowned IP. Even decades after spending my hard earned weekly allowance in the arcades on Missile Command, Asteroids and Super Breakout, I can count myself among the millions that are downloading these games on iOS and Android (disclaimer: Atari is a TriplePoint client). You can bet that team Mario will have a lasting impact on consumers and maintain brand recognition that results in downloads 5-10 years down the road.

Losing Share to Angry Birds

Kids everywhere are wearing Angry Birds shirts and socks, while plushies continue to fill the rooms of children around the world. The ~$30 million merchandising/licensing business around this IP is a strong indicator that the property is capturing the mindshare of consumers, certainly at a loss for Mario. This perhaps is the greatest challenge facing Nintendo the longer it waits to nail down and execute a strategy for distribution on iOS and Android. Yet, the company has a history of bringing fans of its various 1st party IP a reason to buy back into the franchises, and the continued power of those brands will no doubt ensure that it continues to sell hardware and games, and that the expanded audiences take notice as well, even if these casual audiences may no longer be willing to purchase a Nintendo gaming device.

Kids everywhere are wearing Angry Birds shirts and socks, while plushies continue to fill the rooms of children around the world. The ~$30 million merchandising/licensing business around this IP is a strong indicator that the property is capturing the mindshare of consumers, certainly at a loss for Mario. This perhaps is the greatest challenge facing Nintendo the longer it waits to nail down and execute a strategy for distribution on iOS and Android. Yet, the company has a history of bringing fans of its various 1st party IP a reason to buy back into the franchises, and the continued power of those brands will no doubt ensure that it continues to sell hardware and games, and that the expanded audiences take notice as well, even if these casual audiences may no longer be willing to purchase a Nintendo gaming device.

When all is said and done, nothing can sway Nintendo from sitting on its bankroll to continue attempts at innovating gaming fun as we know it, not as long as the market opportunities in mobile fall short of the rewards of maintaining its own closed gaming platform. A company that has over 120 years of history shouldn’t be swayed so easily by market pressures to ditch its game-focused platform for a new market that has been hot during the past 4 years (App Store launched in 2008). A survivor of the turbulent gaming market in the 90s and one that has stood up to Microsoft and Sony, we should be cheering on Nintendo to come up with a fresh gaming experience that takes us beyond a simple touchscreen interface dominated by a company that (understandably) deprioritizes gaming among all forms of digital media. Mario and team may one day land on our mobile devices, but considerations for its existing business should be taken into account, and we’ll always be ready to download Nintendo’s games years down the road.

Pebble is the most notable company to enter this space with a splash, setting the tone for how smartwatch design married with tech can get tech enthusiasts excited. Its move to

Pebble is the most notable company to enter this space with a splash, setting the tone for how smartwatch design married with tech can get tech enthusiasts excited. Its move to  Samsung is another major player taking this space seriously, coming out with its own Galaxy Smartwatch line. Most recently, the company revealed a whole slew of

Samsung is another major player taking this space seriously, coming out with its own Galaxy Smartwatch line. Most recently, the company revealed a whole slew of  We need to completely change the notion of a smartwatch as an accessory to the smartphone, but a piece of technology that is convenient to use and solves common problems in our everyday lives. We once thought that feature phones were an amazing piece of technology that couldn’t possibly get any better, until color screens with web browsing capabilities, improved data bandwidth, and eventually the iPhone came along to change our perception of cellular phones and becoming a necessity, not a “want.”

We need to completely change the notion of a smartwatch as an accessory to the smartphone, but a piece of technology that is convenient to use and solves common problems in our everyday lives. We once thought that feature phones were an amazing piece of technology that couldn’t possibly get any better, until color screens with web browsing capabilities, improved data bandwidth, and eventually the iPhone came along to change our perception of cellular phones and becoming a necessity, not a “want.”

Attending the show also gave us a new level of insight on the regulation that video game companies face while operating in the country – regulating time spent in-game and fighting “addiction”. We’ve heard whispers before, but faced the reality while speaking with others at the show – developers must reduce rewards earned in an online game by 50% upon hitting the 3 hour mark within a 24 hour period, and 100% at the 5 hour playtime mark. It’s inconceivable for a Western developer to imagine operating under these constraints, as the “whales” are publicly and clearly identified for spending the most amount of money over extended daily gaming sessions (see

Attending the show also gave us a new level of insight on the regulation that video game companies face while operating in the country – regulating time spent in-game and fighting “addiction”. We’ve heard whispers before, but faced the reality while speaking with others at the show – developers must reduce rewards earned in an online game by 50% upon hitting the 3 hour mark within a 24 hour period, and 100% at the 5 hour playtime mark. It’s inconceivable for a Western developer to imagine operating under these constraints, as the “whales” are publicly and clearly identified for spending the most amount of money over extended daily gaming sessions (see